Mortgage Investment Corporation Things To Know Before You Buy

Mortgage Investment Corporation Things To Know Before You Buy

Blog Article

Facts About Mortgage Investment Corporation Revealed

Table of ContentsThe Basic Principles Of Mortgage Investment Corporation The Single Strategy To Use For Mortgage Investment CorporationExamine This Report on Mortgage Investment CorporationThe Best Strategy To Use For Mortgage Investment CorporationThe smart Trick of Mortgage Investment Corporation That Nobody is Talking About

Does the MICs debt committee evaluation each home loan? In most situations, mortgage brokers handle MICs. The broker must not act as a member of the credit scores board, as this puts him/her in a direct dispute of rate of interest provided that brokers normally earn a payment for placing the home mortgages. 3. Do the directors, members of credit report committee and fund manager have their very own funds spent? An of course to this question does not supply a safe investment, it ought to supply some enhanced safety and security if assessed in conjunction with other prudent financing plans.Is the MIC levered? The financial organization will certainly accept certain mortgages possessed by the MIC as safety for a line of credit history.

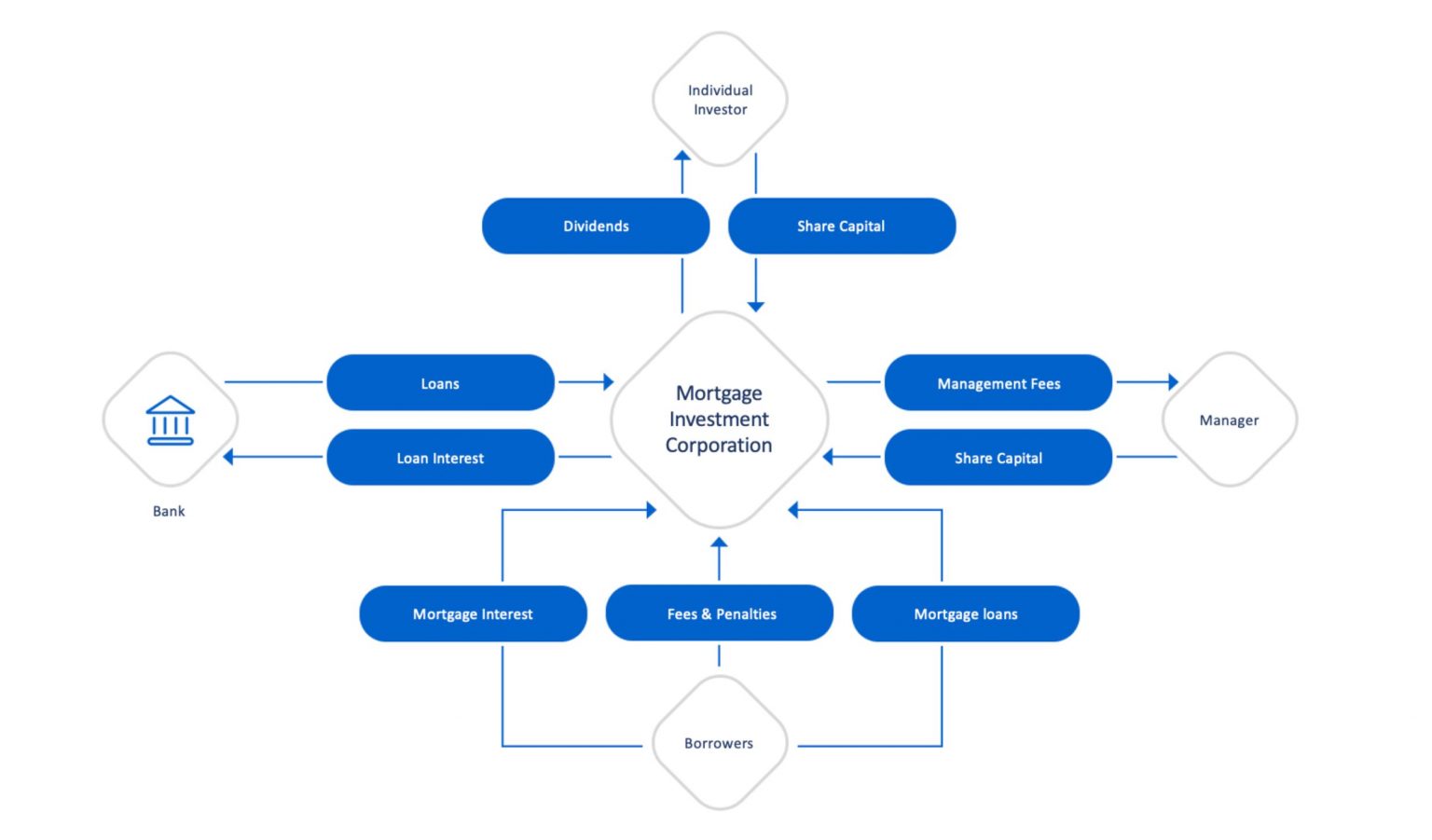

Last upgraded: Nov. 14, 2018 Few financial investments are as helpful as a Home mortgage Financial Investment Corporation (MIC), when it concerns returns and tax obligation advantages. Due to the fact that of their company structure, MICs do not pay earnings tax and are legitimately mandated to distribute every one of their revenues to investors. On top of that, MIC dividend payments are treated as interest earnings for tax objectives.

This does not imply there are not risks, yet, generally speaking, no issue what the more comprehensive securities market is doing, the Canadian real estate market, specifically significant cities like Toronto, Vancouver, and Montreal executes well. A MIC is a corporation formed under the regulations establish out in the Income Tax Act, Area 130.1.

The MIC earns income from those home loans on interest fees and basic charges. The real allure of a Mortgage Financial Investment Corporation is the yield it provides capitalists contrasted to various other fixed revenue investments - Mortgage Investment Corporation. You will have no difficulty discovering a GIC that pays 2% for a 1 year term, as government bonds are equally as reduced

The Definitive Guide to Mortgage Investment Corporation

There are strict requirements under the Revenue Tax Obligation Act that a firm must fulfill before it certifies as a MIC. A MIC should be a Canadian corporation and it have to invest its funds in mortgages. As a matter of fact, MICs are not this content enabled to manage or create property home. That said, there are times when the MIC ends up possessing the mortgaged residential or commercial property due to repossession, sale arrangement, etc.

MICs concern common and favored shares, issuing redeemable favored shares to shareholders with a fixed reward rate. In a lot of cases, these shares are thought about to be "qualified financial investments" for deferred income plans. web link Mortgage Investment Corporation. This is optimal for investors who purchase Mortgage Investment Firm shares with a self-directed licensed retired life cost savings plan (RRSP), signed up retired life earnings fund (RRIF), tax-free cost savings account (TFSA), postponed profit-sharing plan (DPSP), registered education savings strategy (RESP), or registered special needs cost savings strategy (RDSP)

The Ultimate Guide To Mortgage Investment Corporation

And Deferred Strategies do not pay any tax obligation on the rate of interest they are approximated to obtain. That said, those that hold TFSAs and annuitants of RRSPs or RRIFs may be struck with certain penalty tax obligations if the investment in the MIC is considered to be a "prohibited financial investment" according to copyright's tax code.

They will certainly ensure you have actually found a Home loan Financial investment Firm with "professional investment" status. If the MIC qualifies, it might be very valuable come tax obligation time given that the MIC does not pay tax obligation on the rate of interest income and neither does the Deferred Strategy. Much more extensively, if the MIC stops working to fulfill the requirements laid out by the Revenue Tax Act, the MICs income will certainly be strained before it obtains dispersed these details to investors, reducing returns dramatically.

A number of these risks can be reduced though by talking with a tax obligation consultant and investment agent. FBC has actually functioned exclusively with Canadian little business owners, business owners, capitalists, ranch drivers, and independent specialists for over 65 years. Over that time, we have helped 10s of countless customers from throughout the country prepare and submit their tax obligations.

The Only Guide for Mortgage Investment Corporation

It appears both the realty and stock markets in copyright go to perpetuity highs On the other hand returns on bonds and GICs are still near document lows. Also cash money is shedding its allure because power and food costs have pressed the rising cost of living rate to a multi-year high. Which begs the question: Where can we still locate worth? Well I think I have the answer! In May I blogged concerning checking into home mortgage financial investment companies.

If rate of interest rise, a MIC's return would additionally enhance because greater home loan prices mean more revenue! People that spend in a home mortgage investment firm do not possess the property. MIC investors just generate income from the enviable position of being a lending institution! It resembles peer to peer lending in the united state, Estonia, or various other parts of Europe, other than every funding in a MIC is safeguarded by actual home.

Lots of tough functioning Canadians that want to acquire a residence can not get home loans from typical financial institutions due to the fact that probably they're self employed, or don't have an established credit history. Or possibly they desire a short-term finance to create a big building or make some remodellings. Banks have a tendency to neglect these possible borrowers because self used Canadians do not have secure earnings.

Report this page